DIFC Q1 2026 Market Report: Offices & Prices

DIFC Q1 2026 opened with 775 new company registrations, a 62% annual increase announced by His Highness Sheikh Maktoum, igniting renewed demand for office space, boosting professional services and shaping the investment outlook for prime Dubai real estate in the opening months of 2026.

DIFC's early 2026 performance, as reported in the DIFC press release and government statements, indicates material corporate relocation and formation in fintech, asset management and professional services that is translating into stronger leasing enquiries and rental pressure inside the financial district. These flows are drawing investor attention back to core commercial-grade offices and to residential neighbourhoods that serve high-earning professionals.

At the same time, Dubai Land Department transaction data and RERA rental indexes show continued activity across the emirate, with yields and financing costs determining investor strategy. This report breaks down the headline numbers, explains office-market drivers, compares residential price and yield patterns, and highlights risks and financing points every investor should monitor now.

What were the DIFC Q1 2026 market numbers?

What were the DIFC Q1 2026 market numbers? — Key Data

New Companies

775

Annual Growth

62%

Avg DIFC Rent

AED 220-240/sqft/yr

Leasing Enquiries

+25-35%

Direct answer: DIFC recorded 775 new company registrations in Q1 2026, a 62% year-on-year increase announced by DIFC and quoted by His Highness Sheikh Maktoum, with a measurable uptick in leasing enquiries and professional services expansion that is tightening prime office availability and influencing rent and yield expectations across the district.

Elaboration: The 775 new companies figure is the headline metric investors are using to quantify DIFC’s restart momentum; DIFC said the growth was concentrated in financial services, legal, and fintech firms and reflected strong inward interest from Europe and Asia. Local brokers report that leasing enquiries in DIFC are up roughly 25-35% compared with Q1 2025, putting upward pressure on prime headline office rents, which market reports place near AED 220-240 per sq ft per year in Grade A pockets of the district. For investors, the combination of higher leasing demand and limited immediate new office supply implies near-term rental growth and potential revaluation of income-capitalised office assets.

Further detail: Beyond headline registrations, DIFC’s Q1 performance should be read alongside Dubai Land Department transaction trends and RERA rental indices: pockets serving DIFC employees such as Downtown Dubai and Business Bay have seen transactional momentum and rental uplift. The shift from headline registrations to actual leased square footage matters: vacancy compression will determine whether yields compress from current levels. For context, market agents currently price near-term prime office yields in central Dubai office clusters at approximately 5.0% to 6.5% depending on location and lease profile, while smaller boutique office units can yield closer to 7.0% if acquired at attractive pricing and leased quickly.

What were the DIFC Q1 2026 market numbers?

Why is DIFC office demand rising in Q1 2026?

Direct answer: DIFC office demand rose in Q1 2026 because a wave of new company registrations, renewed international relocations and expansion of financial and professional services firms increased leasing enquiries, while limited Grade A new supply in the short term has pushed effective demand into higher headline rents and shorter vacancy cycles.

Elaboration: The Q1 surge stems from three connected drivers: corporate formation and relocation, sectoral growth in fintech and asset management, and secondary effects from policy and events that promote Dubai as a gateway for capital. DIFC’s announcement of 775 new companies and a 62% annual rise is consistent with anecdotal evidence from market agents who report a 20% to 35% uptick in viewings for 1,000 to 5,000 sq ft office suites. Brokers and independent reports indicate prime DIFC headline rents in the AED 220-240 per sq ft per year range, while flexible workspace providers are commanding premium per-desk rates, improving short-term revenue profiles for owners who can convert or sublet space.

Further detail with developer and community comparison: Investors should separate core asset plays in DIFC from overflow demand that benefits nearby communities such as Downtown Dubai and Business Bay. Core DIFC investments tend to secure longer corporate leases with multinational tenants, while spillover demand supports serviced offices and apartments nearby. Typical yields for well-let Grade A DIFC offices are estimated at around 5.0% to 6.0%, while yield-seeking investors in adjacent Business Bay can structure higher initial returns, commonly 6.0% to 7.0%, depending on asset condition and tenant mix. These dynamics make DIFC attractive for income investors seeking corporate leases and for strategic value buyers betting on longer-term capital appreciation.

Why is DIFC office demand rising in Q1 2026?

| Community | Approx Avg Rent (AED/sqft/yr) | Estimated Avg Yield |

|---|---|---|

| DIFC | AED 220-240 | 5.0%-6.0% |

| Business Bay | AED 140-170 | 6.0%-7.0% |

| Downtown Dubai | AED 160-190 | 5.5%-6.5% |

| Dubai International Financial Centre spillover | Varies by building | 5.5%-7.0% |

"DIFC’s Q1 momentum is a demand signal that will sustain leasing activity and push landlords to reconfigure underutilised floor plates into flexible, higher-yield formats."

— Senior Market Analyst, Binayah Properties

What are Dubai residential price trends and yields after Q1 2026?

Direct answer: After Q1 2026, Dubai residential prices continued to show positive momentum with prime pockets such as Downtown Dubai and Dubai Marina registering price gains and yields ranging from roughly 5.5% to 7.0% depending on unit type and location, while Business Bay and newly completed districts offer slightly higher gross yields for buyers focused on rental income.

Elaboration: Residential demand is reacting to commercial-led inflows and to broader macro factors including interest rates and expatriate hiring. RERA rent indices and DLD transaction activity signal that secondary market prices climbed in Q1, with villas and townhouses in family-oriented communities recording steady appreciation and apartments in central locations attracting strong leasing interest. Typical example figures used by market participants in Q1 2026: average one-bedroom apartment sale prices in Downtown Dubai around AED 1.0M to AED 1.5M, with gross rental yields near 5.5% to 6.2%; Business Bay one-bedroom prices nearer AED 800k to AED 1.1M with yields commonly 6.0% to 7.0%. Dubai Marina and Jumeirah Beach Residence carry similar demand patterns for young professionals and short-term leasing.

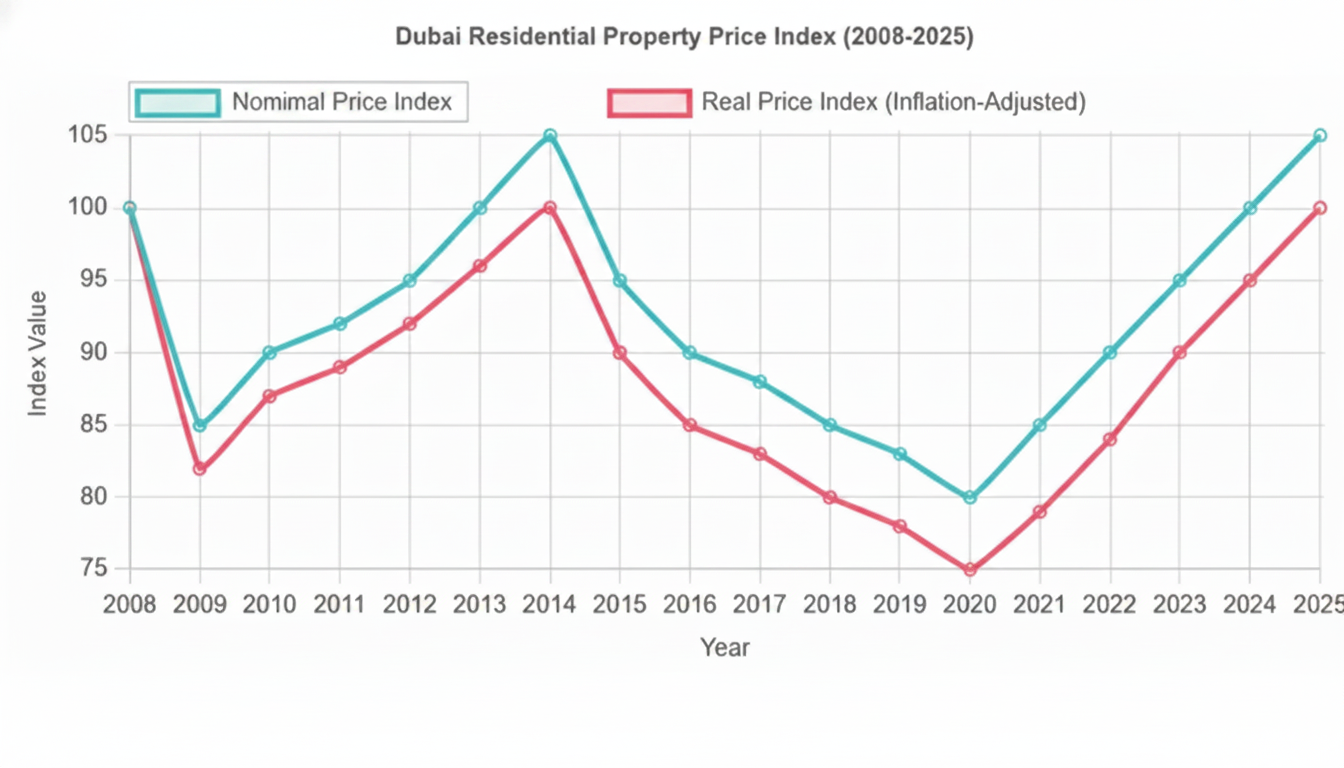

Further detail and implications for investors: Price appreciation has been uneven, favouring limited-supply, high-amenity communities and well-located buildings by top developers such as Emaar, Damac and Nakheel. For income investors, net yields after service charges and management costs typically reduce gross yields by 0.8 to 1.5 percentage points, so a quoted gross yield of 6.5% in Business Bay can translate to a net yield of roughly 5.0% to 5.7% depending on tenant mix and occupancy. Rising mortgage rates and transaction costs can compress investor returns, so investors should model cashflow using conservative vacancy assumptions and include DLD transfer fees, developer service charges and anticipated maintenance. The chart below tracks the price index trend for Dubai over five quarters to show recent trajectory.

What are Dubai residential price trends and yields after Q1 2026?

Dubai Residential Price Index: Q1 2025 to Q1 2026

Indexed price movement across Dubai residential market, baselined to Q1 2025 = 100.

What risks and financing issues should investors watch in 2026?

Direct answer: Key risks for 2026 include rising financing costs and mortgage rates, potential yield compression in core office assets as prices re-rate, and localized supply coming online that can pressure rents; investors must model an average mortgage rate nearer 5.75% and account for Dubai Land Department transfer fees of 4% plus transaction costs when assessing returns.

Elaboration: Interest-rate dynamics are central to strategy now. UAE Central Bank-influenced commercial lending and bank mortgage pricing moved higher through late 2025 and into Q1 2026, with market-reference mortgage rates near 5.5% to 6.0% for typical residential profiles and commercial lending slightly higher depending on borrower risk. Higher rates increase financing costs and push required yields up for buyers relying on leverage. Investors using 70% LTV or higher should stress-test cashflows at lending rates of 6.0% to 7.5% to understand coverage ratios. Transaction costs are also material: Dubai Land Department transfer fees typically 4.0% of the property value plus registration and agent fees can add another 1.0% to 1.5% in upfront costs, which must be included in yield and payback calculations.

Further detail and strategic watchpoints: Supply timing matters; several residential and office projects scheduled for delivery in late 2026 and 2027 could moderate rental growth in targeted micro-markets. Currency and geopolitical shifts that reduce foreign capital inflows would also raise local risk premia. For credit-sensitive buyers, fixed-rate mortgage options from UAE banks can cap short-term financing risk but may come with higher upfront margins. Investors should also monitor developer balance sheets and escrow compliance, as project delays can shift investor timelines. Practical mitigation includes selecting buildings and developers with strong track records such as Emaar and Dubai Holding for residential, or selecting well-let office assets in DIFC with multinational tenants for commercial exposure.

What risks and financing issues should investors watch in 2026?

Key Insight

Mortgage stress-test tip: Model financing at a 6.5% lending rate and a 6 to 12 month vacancy buffer when calculating net yields. Include DLD 4% transfer fee and expected service charges of AED 15,000 to AED 35,000 per year for apartments to avoid overstating returns.

- Rising mortgage rates: 5.5%-6.0% (typical Q1 2026)

- DLD transfer fee: 4.0% of property value

- Net yield reduction: 0.8-1.5% from gross yield after costs

- Project deliveries: monitor 2026-2027 completion schedule

Key takeaway: DIFC’s Q1 2026 performance, anchored by 775 new companies and a 62% annual rise, is a clear demand signal for central Dubai offices and a supportive catalyst for nearby residential rental markets; investors who model financing and costs conservatively and prioritise well-located assets are positioned to capture income and capital upside.

Binayah Properties CTA: Contact Binayah Properties to receive a tailored investment briefing that maps DIFC-led demand to specific acquisition opportunities in Downtown Dubai, Business Bay and Dubai Marina. Binayah provides data-backed valuations, access to off-market listings from developers like Emaar and Nakheel, RERA/DLD transaction analyses and financing introductions to UAE banks. Book a consultation to get scenario-based yield models, recommended entry prices in AED, and a step-by-step acquisition plan that aligns with your return and risk profile.

Binayah Editorial

Property Market Analyst

Our editorial team researches Dubai's real estate market, tracking DLD data, developer launches, and investment trends to keep buyers and investors informed.

Ready to Invest in Dubai?

Speak with our analysts about the best opportunities in today's market — free consultation.