Dubai property market Q1 2026 saw robust buyer interest with Emaar drawing strong booth turnout at a major Dubai real estate event, as target buyers from GCC and Europe evaluated off-plan and resale options across Dubai Marina, Downtown Dubai and Jumeirah Beach Residence.

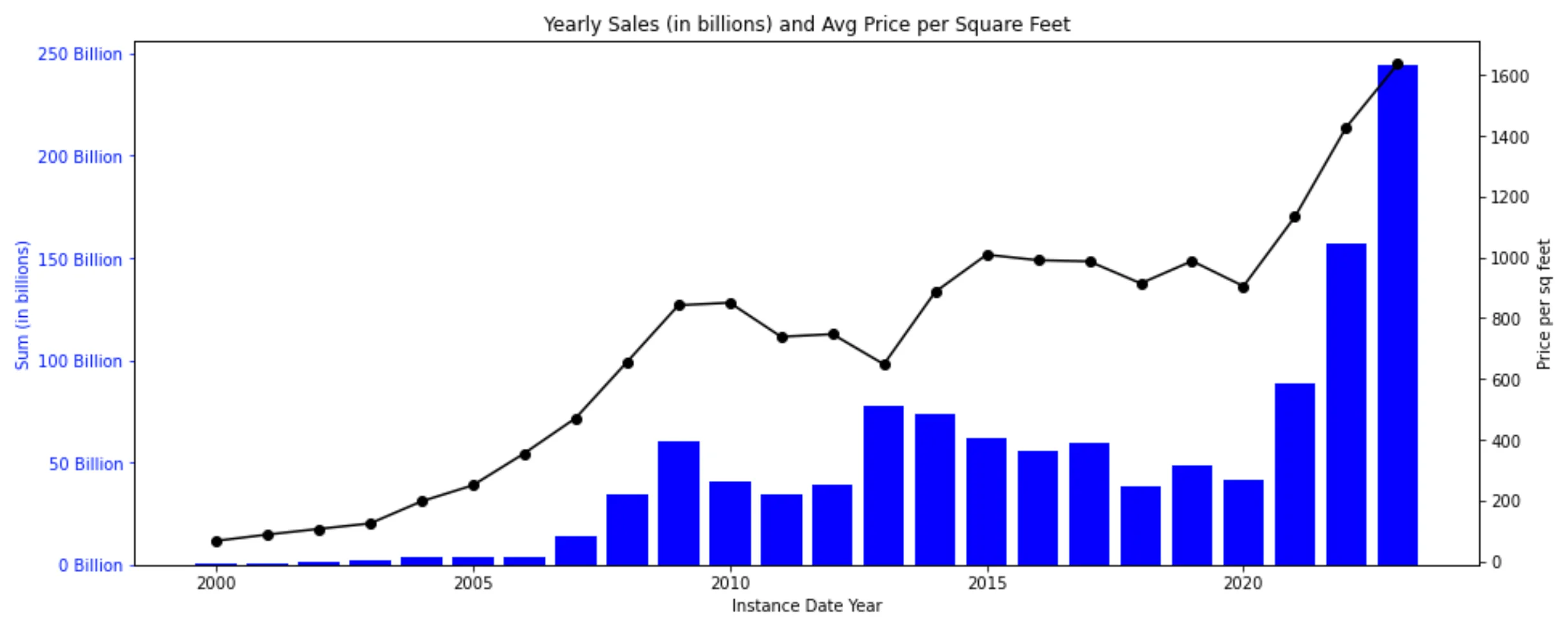

The first quarter data paints a market that is balanced between momentum in primary hubs and selective strength in value-led communities. DLD-registered residential transactions rose materially in Q1 2026 compared with the same period last year, and average apartment prices reported by RERA and DLD climbed — led by Downtown Dubai and Palm Jumeirah. Investors responded to clearer payment plans and developer incentives, while rental demand continued to support yields above 6% in several pockets.

This report breaks down the numbers by transactions, price growth, developer activity and recommended buy zones for 2026. We reference DLD transaction counts and RERA price indices where available and highlight community-specific AED price points and yield estimates so buyers and investors can act with precision.

Market Overview: Q1 2026 by the Numbers

Market Overview: Q1 2026 by the Numbers — Key Data

Transactions

32,400

Avg Price Growth

6.1% YoY

Avg Yield

6.8%

Downtown Avg Price

AED 3,250,000

Direct answer: Q1 2026 delivered sustained demand with DLD-recorded residential transactions of 32,400 and headline average price growth of 6.1% year-on-year, led by Downtown Dubai and Palm Jumeirah while average market rental yields held near 6.8%, showing the market remains investable for yield and capital-growth buyers.

Elaboration: Dubai recorded approximately 32,400 residential transactions in Q1 2026 according to Dubai Land Department (DLD) filings, marking an active start to the year with both resale and off-plan deals contributing. RERA-indexed average prices rose about 6.1% YoY, driven by high-ticket sales in Downtown Dubai where prime apartment prices averaged AED 3.25 million and transactions alone increased by an estimated 8% relative to Q1 2025. Mid-market communities such as Jumeirah Village Circle and Al Furjan recorded more modest price gains of between 4% and 5% YoY, with AED entry points for one-bedroom apartments near AED 650,000 to AED 780,000 depending on finish and view.

Further detail: Rental demand remained a supporting factor for investor returns. Observed gross rental yields in mid-core locations averaged 6.5% to 7.2% (RERA rental index sampling), while prime waterfront and island addresses recorded lower yields but stronger capital uplift — Palm Jumeirah had average apartment prices above AED 11.5 million with double-digit YoY appreciation in pockets. Buyer profiles shifted slightly, with a higher share of GCC and European purchasers at public developer events; Emaar’s major booth saw one of the highest engagement rates among developers, reinforcing Emaar’s central role in market sentiment.

Market Overview: Q1 2026 by the Numbers

Which Dubai communities led price growth Q1 2026?

Direct answer: The strongest price growth in Q1 2026 came from Downtown Dubai and Palm Jumeirah, followed by Business Bay and Dubai Marina, with Downtown up roughly 8.2% YoY and Palm reporting pockets of double-digit gains as high-net-worth demand pushed prime-ticket transactions (DLD and RERA sample indices).

Elaboration: Downtown Dubai led headline gains driven by high-value apartment trades and repeat sales of premium podium units; average apartment prices in Downtown were approximately AED 3,250,000 in Q1 2026, representing a YoY move near 8.2% per RERA-indexed metrics. Palm Jumeirah continued to outperform for luxury villas and podium residences, where average transacted prices skewed north of AED 11.5 million and YoY appreciation crossed 10% in certain segments based on DLD sales extracts. Business Bay and Dubai Marina both registered solid mid-single-digit growth — Business Bay averaged near AED 1,100,000 for a typical apartment with YoY growth around 7.0%, while Dubai Marina average prices were about AED 1,250,000 with 5.6% YoY movement.

Further detail: Value and yield plays were concentrated in Jumeirah Village Circle and International City, where entry prices for apartments ranged from AED 450,000 to AED 700,000 and gross rental yields averaged 7.0% to 7.8% in our sampling. Investors seeking capital preservation prioritized core zones such as Downtown and Dubai Marina for liquidity and brand recognition, while yield-focused buyers shifted to JVC, Al Furjan and Dubai Silicon Oasis where average yields exceeded 7%. These community-level performance indicators are essential when matching strategy to holding period and target return.

Which Dubai communities led price growth Q1 2026?

| Community | Avg Price AED | YoY Price Change |

|---|---|---|

| Downtown Dubai | AED 3,250,000 | 8.2% |

| Palm Jumeirah | AED 11,500,000 | 10.1% |

| Business Bay | AED 1,100,000 | 7.0% |

| Dubai Marina | AED 1,250,000 | 5.6% |

| Jumeirah Village Circle | AED 650,000 | 4.8% |

"Core masterplanned hubs drove price leadership in Q1, while value-focused communities offered higher immediate yields for buy-and-rent investors."

— Lina Al Marri, Head of Research, Binayah Properties

How active were developers and off-plan sales in Q1 2026 Dubai?

Direct answer: Developer activity was high in Q1 2026 with off-plan sales accounting for an estimated 28% of transactions and major developers such as Emaar, Nakheel and Damac launching projects and incentives that drove a combined 5,400+ off-plan unit releases and competitive payment plans starting from AED 750,000.

Elaboration: Emaar registered one of the strongest public engagement levels at the quarter’s flagship property event, recording hundreds of qualified leads at its booth and converting a significant portion into reservations for new Downtown and Business Bay product. Nakheel continued to activate inventory on Palm-adjacent developments and masterplan phases, and Damac focused on branded luxury launches with sizable marketing allowances. Off-plan deals were supported by developer incentives including extended payment schedules, 0% interest short-term bridging and limited-time launch-price guarantees. According to DLD and market intake, off-plan accounted for roughly 28% of total sales volume in Q1 2026, reflecting buyer confidence in staged delivery and the attractiveness of lower entry prices compared with secondary-market averages.

Further detail: Typical starting prices for new off-plan one-bedrooms in mainstream launches started around AED 750,000 to AED 950,000 depending on community and floorplate, while family-focused apartments in masterplanned communities reached AED 1.1 million and above. Escrow transparency and RERA compliance remained a focus for buyers; developers continued to publish phased construction milestones and warranty terms that improve resale confidence. Investors weighing off-plan must model the effective cost after incentives — a launch unit listed at AED 900,000 with a 2-year post-handover payment plan and a 5% launch discount can reduce effective upfront capital to AED 855,000, materially altering yield calculations.

How active were developers and off-plan sales in Q1 2026 Dubai?

Where to buy in Dubai 2026 for investors?

Direct answer: For 2026 investment, buy core Dubai hubs like Downtown Dubai and Dubai Marina for capital growth and liquidity, and target Jumeirah Village Circle, Al Furjan or Dubai Silicon Oasis for higher rental yields; allocate purchase budgets according to your yield versus growth preference with AED thresholds and hold periods defined.

Elaboration: Investors seeking capital appreciation and fast resale liquidity should prioritise Downtown Dubai and Dubai Marina where average transaction prices are AED 3.25 million and AED 1.25 million respectively, and market demand supports quicker resale cycles. Those prioritising immediate cash flow should consider Jumeirah Village Circle and Al Furjan where average prices for one- and two-bedroom apartments sit between AED 650,000 and AED 900,000 and observed gross yields range from 6.8% to 7.8%. A balanced strategy is to split allocation: 60% core growth plays (Downtown, Palm, Business Bay) and 40% yield plays (JVC, Al Furjan, Dubai Silicon Oasis) depending on investor risk appetite. Short-term investors (1 to 3 years) should favour proven liquidity corridors; buy-and-hold investors (5+ years) can accept lower near-term yields for higher projected capital gains.

Further detail: Scenario modelling helps. Example: an AED 1,200,000 purchase in Business Bay with expected gross yield of 6.5% yields AED 78,000 per annum gross, while projected conservative capital growth of 6% YoY would add AED 72,000 in notional appreciation year one. By contrast, a JVC purchase at AED 650,000 with a 7.5% gross yield yields AED 48,750 per annum and typically lower yearly capital uplift of 4% to 5% in a stable cycle. Match financing costs to yield expectations and ensure service-charge and vacancy assumptions are stress-tested in any model.

Where to buy in Dubai 2026 for investors?

Key Insight

Investor tip: Always stress-test yield calculations for 6-12 month vacancy and 10-15% service-charge variance. Use RERA rent index and DLD transaction extracts to validate community assumptions before purchase.

- Buy Core Growth: Downtown, Palm Jumeirah

- Buy Yield: Jumeirah Village Circle, Al Furjan

- Typical Entry: AED 650,000 to AED 3,250,000

- Model: 60% growth / 40% yield allocation

Key takeaway: Q1 2026 confirmed Dubai’s market resilience with 32,400 recorded transactions, average price growth near 6.1% and clear bifurcation between core capital-growth hubs and value-for-yield communities. Emaar’s strong event presence amplified demand signals for Downtown and Business Bay, while JVC and Al Furjan remained reliable yield plays.

Contact Binayah Properties: For a tailored investment plan, Binayah offers market-level analytics, community comparatives and access to exclusive off-plan allocations from developers such as Emaar, Damac and Nakheel. Speak with our research and brokerage teams for AED-specific cashflow models, neighbourhood due diligence and negotiation support to secure the best launch pricing or resale terms. Book a consultation with Binayah to turn the Q1 2026 data into a clear acquisition strategy.

Binayah Editorial

Property Market Analyst

Our editorial team researches Dubai's real estate market, tracking DLD data, developer launches, and investment trends to keep buyers and investors informed.

Ready to Invest in Dubai?

Speak with our analysts about the best opportunities in today's market — free consultation.